📘 Explainer · June 23, 2026

Beyond Chips and Models: Why German Energy Infrastructure Companies May Be the Quiet Architects of AI Progress

In the global contest for artificial intelligence leadership, attention fixates on GPUs, foundation models, and the hyperscalers pouring billions into training clusters. The more consequential constraint, however, is measured in megawatts, not teraflops.

In the global contest for artificial intelligence leadership, attention fixates on GPUs, foundation models, and the hyperscalers pouring billions into training clusters. The more consequential constraint, however, is measured in megawatts, not teraflops. AI workloads are extraordinarily power-intensive, and the physical systems required to generate, transform, transmit, and stabilize that electricity are now the binding bottleneck. German industrial companies, with deep expertise in large rotating equipment, high-voltage infrastructure, and nuclear-adjacent technologies, are emerging as essential—yet still underappreciated—players in this new phase of the AI race.

The numbers are stark. According to the International Energy Agency’s base case, global data center electricity consumption is projected to roughly double to around 945 TWh by 2030, representing just under 3% of total global electricity use. Growth is running at approximately 15% annually—more than four times the pace of overall electricity demand. Accelerated servers, driven primarily by AI, are expected to grow at 30% per year and account for nearly half the net increase in data center power consumption. The United States alone is forecast to see data center demand rise by around 240 TWh (+130%) by 2030; Europe is projected to add more than 45 TWh (+70%).

Goldman Sachs estimates data center power demand will grow 160% by 2030, with AI contributing roughly 200 TWh of incremental annual global consumption by the end of the decade. Some scenarios put U.S. data centers at 11–12% of national electricity consumption by 2030. These are not marginal increments; they represent load growth equivalent to adding the entire current electricity demand of mid-sized industrial economies in just a few years.

The Bottleneck Has Shifted from Silicon to Steel and Copper

While chip supply chains have scaled impressively, the power system has not. Large power transformers—critical for stepping voltage between generation, transmission, and data center substations—now face lead times of up to four years for high-capacity units, up from roughly two years pre-2020. Demand for generator step-up transformers in the U.S. surged 274% between 2019 and 2025; substation transformer demand rose 116%, fueled by AI data centers, electrification, and renewables.

Prices for key components have increased roughly 80% over five years. Reports indicate that 30–50% of planned U.S. data center capacity slated for 2026 (approximately 7 GW out of 12 GW announced) faces delay or cancellation risk due to transformer shortages and grid interconnection queues. Hyperscalers are increasingly turning to on-site generation precisely to bypass these multi-year grid delays.

This is the domain where German engineering has long held comparative advantage: precision manufacturing of heavy electrical equipment, high-reliability turbines, and grid stabilization technologies. The mismatch between short-cycle digital hardware and long-cycle physical infrastructure is now dictating project timelines worldwide.

Siemens Energy: Deeply Embedded in the Power-AI Nexus

Siemens Energy stands at the center of this intersection. In fiscal 2025 the company generated €39.1 billion in revenue with approximately 103,000–105,000 employees globally. By Q2 FY2026 it reported a record order backlog of €154 billion, with strong book-to-bill ratios and upgraded guidance for 14–16% comparable revenue growth and 10–12% profit margins before special items.

Two divisions are particularly relevant:

-

Grid Technologies has seen exceptional demand, including for transformers and grid solutions, with notable contribution from U.S. data center-driven orders. The segment has posted double-digit revenue growth and record backlog (reported at €49 billion in one recent update), prompting raised segment guidance. Siemens is actively expanding U.S. manufacturing capacity, including a major transformer facility investment in Charlotte, North Carolina.

-

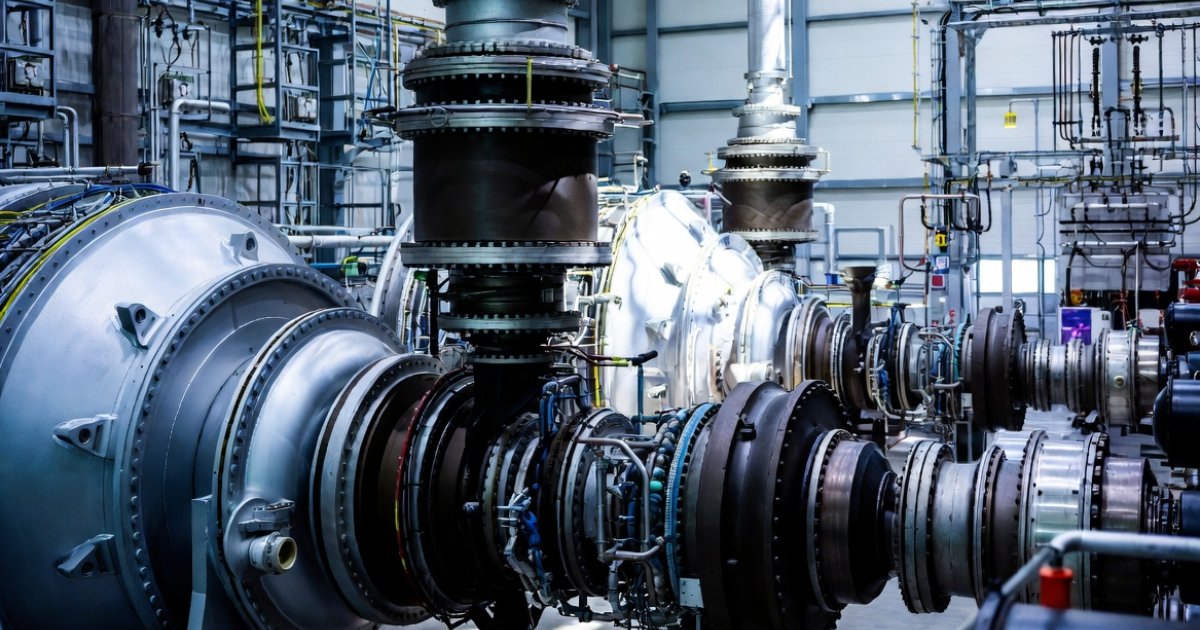

Gas Services supplies fast-starting gas turbines (including the SGT-800 class at 45–62 MW and larger frames up to hundreds of MW) ideal for backup, peaking, or behind-the-meter generation at data centers. The company explicitly markets integrated data center power solutions encompassing grid connection, power transformers, battery energy storage (BESS), STATCOMs and synchronous condensers for voltage stability and load fluctuation management, and fast-start generation.

On the nuclear side, Siemens Energy brings more than 60 years of sector experience. It supplies steam turbines, generators, and electrical balance-of-plant equipment for both large reactors and small modular reactors (SMRs). Recent activity includes a partnership with Rolls-Royce SMR to provide turbine island systems and support for U.S. nuclear recommissioning projects (e.g., with Holtec). Even after Germany’s 2023 nuclear phase-out, the accumulated know-how in high-integrity rotating equipment, generators, transformers, and plant auxiliaries (including cooling and balance-of-plant systems) positions the company to participate in the global revival of interest in firm, low-carbon power for AI loads.

Market observers have noted the shift: one prominent German financial commentator highlighted Siemens Energy as an “AI star” benefiting from the need to build power grids for AI electricity demand, with its stock at times outperforming pure-play AI names since late 2023. Anecdotal reports suggest a high share of recent gas turbine orders tied directly to data center needs.

Germany’s Broader Position: Industrial Strength Meets Domestic Headwinds

Germany remains a powerhouse exporter of electrical machinery and electronics, shipping $159 billion in 2024 (sixth globally). Its engineering tradition in high-voltage equipment, precision turbines, and complex power systems is world-class. European data center demand is also rising sharply (+70% by 2030 per IEA), and grid modernization plus new firm power sources are prerequisites for capturing more of the AI value chain.

Yet domestic challenges are real. High electricity prices, slower permitting timelines compared with parts of the U.S., and the legacy effects of the nuclear phase-out have complicated rapid domestic deployment. Europe as a whole faces a “race to power” where clean resources exist but aligning supply, infrastructure, and speed remains difficult. In the AI context, this means German firms are often stronger as global exporters and technology providers than as anchors of Europe’s own hyperscale buildout.

The “Unseen Heroes” Thesis Holds Analytical Weight

The hypothesis that German energy infrastructure companies could be the unseen heroes of the AI race is not hype—it is a structural observation. AI progress ultimately depends on reliable, high-quality electrons delivered at scale and on time. The companies that manufacture the turbines for flexible or on-site generation, the transformers that move power across strained grids, the grid stabilization systems that maintain power quality under variable AI loads, and the nuclear-grade equipment for new firm-power projects are few in number and operate on multi-year cycles.

Siemens Energy combines all these elements under one roof, with active U.S. localization, a record backlog providing visibility, and explicit positioning in data center power solutions plus nuclear supply chains. While American (GE Vernova), Japanese, Swiss/Swedish (ABB/Hitachi Energy), and Chinese players also compete—particularly on volume transformers—the combination of integrated offerings, reputation for reliability in mission-critical applications, and nuclear-adjacent expertise gives German capabilities distinct relevance at a moment when hyperscalers are signing nuclear restart and SMR deals for 24/7 carbon-free power.

The AI race is visibly about models and chips. Invisibly, it is increasingly about who can energize them. German energy infrastructure firms are not guaranteed to dominate, but they are structurally positioned to be indispensable participants and, in several high-value segments, quiet leaders.

Risks and Strategic Considerations

Execution on the massive backlog, margin pressure from raw material costs and competition, and the ability to localize further amid geopolitical supply-chain scrutiny all matter. Domestically, Germany must address energy affordability and permitting speed if it wants to host more AI infrastructure rather than merely supply it. Globally, Chinese manufacturers are scaling transformer capacity aggressively; Western buyers, however, often prioritize proven reliability and cybersecurity for critical grid assets.

For investors and policymakers, Siemens Energy (and the broader German/European industrial base in power equipment) offers leveraged exposure to the least-discussed but fastest-constraining layer of the AI stack. The winners in AI may ultimately be those who solve the power problem as elegantly as they solve the silicon one.

References

Goldman Sachs. (2024, May 14). AI is poised to drive 160% increase in data center power demand. https://www.goldmansachs.com/insights/articles/AI-poised-to-drive-160-increase-in-power-demand

International Energy Agency. (2025). Energy and AI – Analysis. https://www.iea.org/reports/energy-and-ai/energy-demand-from-ai

pv magazine USA. (2026, May 11). U.S. transformer market faces severe supply constraints as lead times extend to four years. https://pv-magazine-usa.com/2026/05/11/u-s-transformer-market-faces-severe-supply-constraints-as-lead-times-extend-to-four-years/

Siemens Energy. (2026, May). Earnings Release Q2 FY 2026. https://www.siemens-energy.com/us/en/home/press-releases/earnings-release-q2-fy-2026.html

Siemens Energy. (n.d.). Data Center Power Solutions. https://www.siemens-energy.com/us/en/home/products-services/solutions-industry/data-center.html

Additional supporting data drawn from company filings, Wood Mackenzie analyses referenced in industry reporting, and market commentary on supply-chain dynamics (2025–2026).